Weekend Reads: August 22, 2021

WTF Happened in 1971? Becoming a Digital Ghost, Vitamin D Deficiency

Hi folks,

No weekend reads last weekend as I was once again traveling.

I’ve withheld from writing about anything related to the Afghanistan debacle — mostly because I don’t think I have much unique to say. It’s also noteworthy that in moments like these, you are often the target of very specific media campaigns with ulterior motives from conflicting angles and it’s often good to wait for the dust to clear.

I’ve read a few good analyses. The most entertaining one pointed out that the Chairman of the Joint Chiefs of Staff has never fought in combat and, like many of the top figureheads in the American bureaucracy today, is more politician-bureaucrat than practitioner.

This debacle has, though, emboldened my realist’s bull case for Bitcoin. I will likely write on that soon.

Here’s a taste of I’ve found enlightening these past two weeks:

Articles

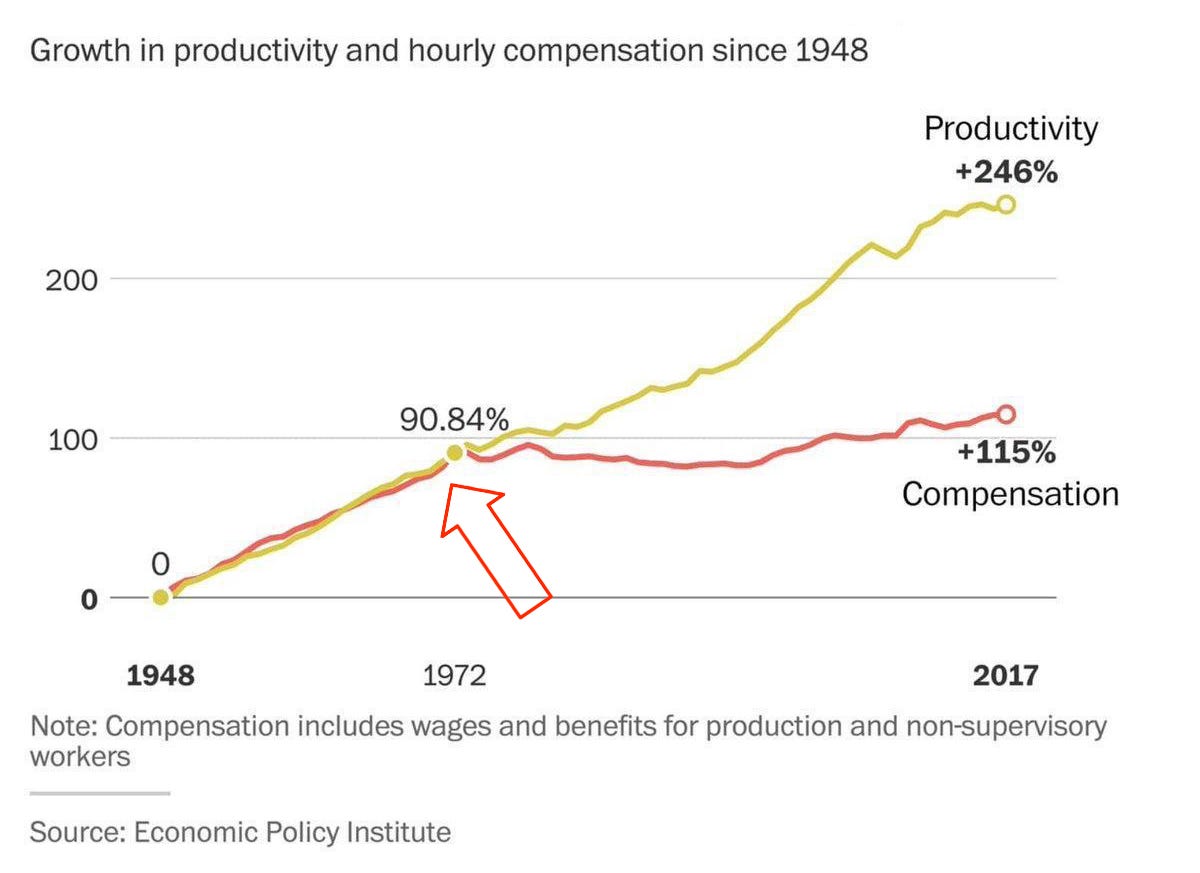

I originally came across this website years ago. I’m revisiting it for a reading group I am hosting for 1517 Fund on WTF Happened in 1971? Or, the Failure of the Elites this fall.

If it isn’t obvious from the ads plastered all over the site, it’s coming from the crypto-goldbug angle with the implicit answer that “Nixon moving us off the gold standard caused a bunch of weird (and generally bad, for most people) macroeconomic effects.” These effects include, most notably, increased inflation in the 1970s and the disjointing of real wages from productivity, among a bunch of other things listed on the website.

I’m not sure it’s that simple — it’s not obvious that Nixon effectively ending the old Bretton Woods system was a cause of these things or an effect of broader macroeconomic movements.

It seems to go hand-in-hand with a broader cultural move from substance to legitimacy that happened in the 1960s and 1970s. You can see this in the rise of credentialing for credentialing’s sake, the move towards new forms of architecture that are promoted largely by architects looking for the approval of other architects, the horrid liturgical movements that did away with organs and chanting and ushered in tambourines and guitars in both protestant and Catholic churches across the world, among other phenomenon.

There certainly is an intuitively believable narrative that moving from hard money that can’t be printed out of thin air to, well, money that can be printed out of thin air has strange effects on how people spend their time and, therefore, their psychology. The Austrian school economists explore this concept extensively, with Ludwig von Mises spending a considerable chunk of Human Action talking about time preferences. Some Bitcoin Maximalists go as far as to pin the blame for almost everything shoddy we see around us today — bad architecture, bad food, bad culture, bad liturgy — on the effect of being less invested in the distant future than in the immediate, near future as an effect of the general devaluation of money.

Perhaps. At the very least, I think this requires a serious reading of the breakdown of Bretton Woods, the devaluation of the pound sterling in that preceded it, and a lot of the other weird cultural effects that were going on in the 1950s and 1960s. A lot of these movements started well before the breakdown of Bretton Woods and started outside the Dollar’s main sphere of influence. I can think of at least two just-as-persuasive arguments about the broader cultural shifts that rely on a reactionary element in society reacting against the horrors of WWII and against the prospective horrors of the Cold War, respectively.

Regardless, WTF Happened in 1971? is fun food for thought.

“How to DELETE Yourself from the Internet and Become a Digital Ghost” on Twitter

I deeply admire those friends and peers of mine who have seemingly disappeared from the face of the earth.

(Ironic, I know, coming from somebody who wrote the book on a non-cringe personal brand.)

My general advice for people who struggle with spending too much time online is to just Log Off. If you don’t need to be on social media for your job, you are almost certainly getting less from it than you think you are. It’s likely sapping your dopamine receptors in your brain, opening you up to multiple avenues of attack from nefarious actors, and opening up your mind to additional attack by parties with concentrated interests in getting you very Worked Up on whatever Outrage of the Week is going around.

This thread will walk you through how to begin the de-personing process. You don’t have to fully de-person, of course. But the more you limit the unnecessary, the more time you can spend on things that actually matter to your life.

“Historical migration and contemporary health” by numerous authors at Oxford Academic Papers

From where your family migrated may affect how likely you are to experience vitamin D deficiency. It appears that people who migrated from sunnier regions to less-sunny regions are more likely to experience vitamin D deficiency than people who are from less-sunny regions.

Vitamin D deficiency may also play a significant role in whether or not children develop food allergies. Researchers found a correlation between birth month (less-sunny months in Fall and Winter) and food allergies.

The former certainly makes sense. There’s an evolutionary trade-off between skin pigmentation and vitamin D synthesis. Dr. Rhonda Patrick has talked about this publicly before. Somalis in Sweden are significantly more likely to experience vitamin D deficiency than native Swedes despite both populations experiencing the same weather.

I would be interested in seeing somebody dig deeper into how well the body absorbs vitamin D supplements. In my limited anecdotal experience, those from sunnier regions seem less-able to absorb vitamin D supplements than somebody like myself, whose ancestors spent probably the last 1200 years in some of the cloudiest regions of Europe.

h/t Alex Tabarrok by way of Michael Gibson

“Other People’s Blood” by Tim Barker @ n+1

This is another reading in our WTF Happened in 1971? workshop. It tackles some effects of the problem of inflation in the 1970s from a left-leaning angle and provides a different perspective in a conversation that is often dominated by people focused on sound money discussions.

Remember this chart from above?

Look at what happened right around 1979-1981.

This sudden pullback in inflation is what is known as the Volcker Shock. It was the effect of the Federal Reserve chairman Paul Volcker’s attempts to reel in the out-of-control inflation of the 1970s. It was quite successful, as you can see above. By the mid-1980s, inflation was more or less under control and by the 1990s, it was near Gold Standard era levels.

Inflation is “good” if you have fixed debt on your books. Your business pulls in more money but your debt more or less stays the same. Even better, you got it with a low interest rate. Your cash grows at a much higher rate than the interest rate, so you can pay it down fast.

(By the flip side, it’s really bad if you’re a creditor with fixed interest rates.)

Deflation, conversely, is bad if your business depends on taking on debt. The higher interest rates that accompany deflation and the decrease in prices means that debt becomes considerably more expensive.

(Very, very cursory explanation of the problem here, not taking into account international pressures.)

The United States in the 1970s and 1980s still had a debt-dependent manufacturing base. Even though Nixon had opened trade to China, there were still significant manufacturing bases in the United States in the south, Pittsburgh, Detroit, and other, smaller enclaves.

The Volcker Shock drove interest rates through the roof. As a consumer oriented example: 30-year mortgage in 1976 only(!) cost 8.87%. In 1981, 16.63% (!!!). Rates didn’t get back to their pre-Volcker Shock levels until 1991.

Increased prime interest rates had a real effect on capital intensive, debt-dependent businesses with low margins that were already facing stiff competition from abroad and increased costs domestically from unionization.

At the height (or nadir) of the Volcker shock, prime interest rates were over 20 percent — and worse if you had bad credit. The exorbitant cost of borrowing put tens of thousands of firms out of business and led overall to twenty-two months of negative growth. In December 1982, unemployment was at 10.8 percent — closer to 20 percent if you include workers who wanted jobs but had stopped looking and underemployed workers who could not find steady full-time work. In absolute terms, twelve million Americans were unemployed that month, plus another thirteen million “discouraged” and underemployed.

The nation’s industrial belt was the hardest hit. Ninety percent of job losses occurred in mining, construction, and manufacturing. It was costly for businesses to pay their debts and borrow money to invest, while a strong dollar made American exports even less competitive internationally. In places like Flint, Michigan and Youngstown, Ohio, more than one in five workers were unemployed. In Akron, the commercial blood bank reduced the prices it would pay by 20 percent due to the glut of laid-off tire workers lining up to bleed. In the area around Pittsburgh, suicide rates and alcoholism soared, while residents competed for spots in homeless shelters. The unemployment rates for African Americans were worse, peaking in early 1983 at 21.2 percent (up from around 12 percent — already a crisis — in 1979).

The Volcker Shock worked but at an immense cost. As talk about higher levels of non-transitory inflation heats up in the US, you can bet the house (please don’t) that Janet Yellen at J Powell know this was an immense cost. That then raises the question: what are the alternatives to get inflation under control?

(fwiw: I’m still in the camp that a lot of the inflation really is transitory and largely a function of supply chain issues — but it’s not obvious just how much is.)

Books

Winning the Loser’s Game: Timeless Strategies for Successful Investing by Charles D. Ellis

This is a good introductory-to-intermediate layperson book on, essentially, index investing. The author does a great job illustrating the costs of active investing and stock-picking over an extended period of time, especially for non-professional investors who don’t have a true competitive advantage in the market.

Sure, there may be some broader structural questions about the effects of index funds on the market, but that’s not the concern of the individual investor trying to make returns for their personal goals. For the individual, non-professional investor, you just need to match the market regularly over a long time-frame in order to get decent returns. That’s largely achieved with low cost index funds and passive investing. You can manage your diversification in your portfolio with index funds from different markets, but generally speaking, you want to avoid actively managed mutual funds with high turnover, high fees, and rarely-met promises of exceeding the market.

I would recommend this light read to any layperson who has already implemented the strategies of somebody like Ramit Sethi into their personal finance regimen but wants to learn more and avoid actively managed mutual funds or stock picking. Sethi and Ellis actually disagree about target date funds versus low cost index funds, but for most people the key takeaway will be to avoid actively managed funds.

Disclosure: My portfolio mostly follows a barbell distribution, with low cost, relatively low risk index funds making up a large chunk on one end, and risky growth stocks on the other end.

No podcasts or videos this week.

Cheers,

Zak