Talent Identification, Venture Capital & Optimism

Or, How Targeted Belief in a Few Outstanding People Moves the Needles of Industry

The following is a (lightly edited) talk I wrote up to give to fellows at American Moment, an organization that identifies, educates, and credentials young Americans who will implement, craft, and influence policy supporting strong families, national sovereignty, and prosperity. I ended up not using this as written and as much as I don’t believe that the world needs another substack bloviating on power laws, I figured some readers of this newsletter may find this interesting.

The American Moment guys asked me to give a talk to you about venture capital. At first, I was a little confused about this, given that this is, I suspect, a policy fellowship. But upon further reflection, it makes sense.

Governments are often some of the biggest stakeholders in venture capital funds, venture capital is often talked about in any conversation about tech and finance, the vast majority of NASDAQ and NYSE traded companies were funded initially with venture capital and employ a growing and substantial portion of the workforce, and, I believe, venture is one of the better-suited tools of governments for economic development (i.e., to give you a point of reference, our portfolio employs more than 500 people, mostly Americans and mostly in high-paying jobs across industries all over the country). Laters stage venture capitalists are also positioned to pressure -- or not pressure -- startups in particular with respect to the initiatives of activist organizations.

Also, a good early stage venture capital fund, like my own, is fundamentally in the human capital business, just like universities. I believe that we’re better at it than the universities, too. More on that later.

So, venture is a unique and interesting asset class from the perspective of the young professional -- and also worth examining closely (or at least understanding) for the policy professional.

As an aside, it’s always interesting to hear policy wonks or journalists talk about venture because you realize they just have no idea what they’re talking about -- just like with most industries journalists like to bloviate upon.

In this short talk, I will run you through what venture capital is as an asset class, who invests in it, what VC funds invest in, what our mandate is, how we can (and cannot) pressure companies, and give you a look behind the curtain at what our job really is. This will better equip you to have intelligent policy conversations about this small but important financial asset class. It should also give you an important advantage in your careers, should you decide to work in the private sector at some point.

You’ve heard me already call venture capital an “asset class.” That is, fundamentally, what it is. Just like stocks, bonds, real estate, or leveraged buyout private equity, it’s a way to deliver returns to investors. I joke with founders that I am nothing more than a glorified mortgage banker. My job is to responsibly deploy capital from investors to recipients of that capital and try to ensure that at least some of those recipients return a certain multiple on that money by a certain date. Except rather than homes it’s companies. And rather than 3.19% per annum over 30 years, it’s more or less at least 3x net fees over 7-10 years.

It’s also a relatively small asset class. Most estimates place it as just a fraction of the trillions managed by private equity funds.

Now, to better understand this asset class, it’s worth asking two questions: for whom do we do we deploy capital? And how do we do this?

For Whom Do We Do This?

Venture capitalists are asset managers. Just like mortgage bankers or hedge fund managers or private equity fund directors, we deploy capital on the behalf of, usually, other people.

(A quick side note: some venture capitalists also deploy their own money and most are expected to deploy at least some of their own money, but most raise and deploy capital on the behalf of other investors.)

Who those other people are depends on the size of the fund, the kinds of investments made by the fund, and the goals and preferences of the general partners (i.e., the bosses) of the fund.

Your larger funds out there, those that manage billions of dollars, such as Sequoia, Kleiner Perkins, a16z, Founders Fund, crossover funds, etc. They raise largely from institutions like university endowments, pension funds, corporate investors, foundations, and sovereign wealth funds. Pension funds and sovereign wealth funds may be particularly interesting to you as those interested in policy.

The former because they’re often public pension funds that are insolvent or borderline insolvent and must chase higher -- but riskier -- returns in order to keep themselves from going under. CalPERS -- California’s pension fund -- is a good example of this.

The latter, sovereign wealth funds, may be interesting because it means that our financial elites are often capitalized by governments with decidedly contrary interests to those of most Americans.

Up until recently, Chinese families were also a large source of capital for the industry. Under new rules implemented by the Committee on Foreign Investment in the United States (CFIUS) during the Trump Administration, it became much harder for Chinese family offices to invest in VC in the US. Much to the chagrin of some investors.

Smaller funds, those managing less than a few hundred million dollars, tend to be funded by an amalgam of sources like high net worth individuals, family offices, maybe some smaller endowments, foundations, or government programs.

Types of Funds

These investors, Limited Partners (or, “LPs” in the lingo of the industry) expect a certain return over a certain date range, depending on the type of fund they invest in.

Funds can generally be broken down into a few categories:

Seed/Pre-seed: writing checks between a few hundred thousand dollars and a million dollars in the earliest stages of the company. These funds have 7-10 year windows and investors expect at least 3x net from top-tier funds. This is the kind of fund I work for. We’re often investing when it’s just a team of cofounders with maybe one or two customers.

Early Stage: writing checks of a few million dollars, with some exceptions for very capital intensive sectors like space exploration or transportation. These funds have 5-7 year windows, typically.

Growth: writing checks of dozens of millions of dollars. By the time a growth fund invests in a company, you may have heard of the company if it is consumer-facing or services your industry or sector. These have shorter time windows. Some hedge funds have started playing in this territory, gobbling up shares of companies before they go public.

Late-stage/Pre-IPO: writing even larger checks, typically getting a company ready to go public. When you get into this territory, you’re typically dealing with investment banks, more hedge funds, and just simply very large institutions that can write larger checks.

Generally speaking, the earlier the stage, the smaller the check, the riskier the investment and the higher the investment return expectation (just like with other asset classes -- riskier bonds have higher yields, growth stocks are riskier but have higher return expectations). That should be obvious enough.

Still, this leaves the question of “how do VC funds try to achieve this” unanswered. The earlier you go, the bigger the return expectations. But the less of a “company” there is there. At the stage my colleagues and I invest, we can’t really run discounted cash flow analyses on a company, can’t analyze the value of its patents through an algorithm, and can’t get a sense for the price of shares of the company on some kind of mostly liquid secondary market.

No, earlier on, this is far more a bet on people -- and that bet is, I think, more art than it is science. This is particularly true at the earlier stages, which is really what I’m best qualified to speak about, so let’s dive in.

Early Stage VC is about Talent Identification

Another joke I tell founders is that my job is far more like that of a sports recruiter than it is a financier. I scour the country trying to find the best talent in technology and the sciences before anybody else can find them. I visit college campuses, work with campus organizations, even try to mentor or give talks to high schoolers. Not (primarily) out of any kind of altruism, but because early stage VC is a bet on people.

This is particularly true for a fund like 1517, which has a very specific and kind of strange founder-focused thesis. Some funds have theses that focus on sector, industry, or stage. Ours is about founders. Even more, it’s about the educational status of the founders. Even weirder, it’s about their educational non-status. We like betting on dropouts, opt-outs, and scientists working outside of academia.

I’m going to try to concretize a lot of early stage VC for you here through the example of what it is we do.

Our thesis comes from the years that my colleagues and our General Partners, Michael and Danielle, were working at the Thiel Foundation. They are the cofounders of the Thiel Fellowship program, along with Peter Thiel, Jim O’Neill, and a few other folks on the team. The Fellowship is now considered a roaring success. Thiel Fellows have produced companies and projects that have a cumulative market value greater than Harvard’s $40bn+ endowment, the early Fellowship had a hit rate better than most venture capital funds, and chances are you’re already benefiting from technologies developed by Fellows.

At the time, this wasn’t the case. Larry Summers, Obama’s Treasury Secretary and the once-president of Harvard, called the Fellowship the “single most misguided act of philanthropy of the last decade.” The idea of paying people to drop out of college was pilloried as reckless and hypocritical for a Stanford alum. And, in general, there were a lot of people rooting for it to fail.

Our firm’s thesis came out of the GPs’ experiences running that fellowship program, identifying talent very early on from across the world and across thousands of data points. And seeing an opportunity in the market -- very few funds would serve a founder profile like that.

And at this stage of the game, you’re often making a bet purely on characteristics of the founders. So, if you’re purely making a bet on leading indicators about a person, most people will of course defer to those with the most prestigious credentials, from the FAANG companies, and with the most experience. It’d be an outlandish bet, but the alternative is to compete on the same metrics everybody else competes on. And as we know from ECON 001, increased competition drives profits closer to zero.

So, profits in this world, just like in other industries, lie on the boundary between the outlandishly risky and the predictably safe. Go too far into the outlandishly risky and you risk destruction. Stay too far inside the predictably safe and inflation or the market or competition eats your profits to zero.

Ironically, I view my work, and the work of extremely early stage investors like myself, as akin to that which a good university does. Unfortunately, even elite universities in the west have become little more than hedge funds with nonprofit real estate attached (i.e., Harvard’s $40bn+ endowment) in the best cases and inadvertent honeypots for espionage and citadels of intellectual corruption in the worst cases.

What I mean is this: if you were charged with starting a university, what would you do? I’d do this -- I would find the best group of edge-case ambitious, hard-working young people whom you know are going to be successful regardless of what they do or do not learn in your university. We have a debate about what traits make somebody successful -- IQ, openness, conscientiousness, etc. -- but you would chose your pet traits and select for those. Do this every year for a few years. After a few years, your alumni will start seeing success.

(It’s debatable how much you really made them successful. I’m in Bryan Caplan’s camp. I think the human capital gains from education are marginal, especially outside of the areas where people regularly use what they learn.)

This creates a virtuous cycle. People are fundamentally mimetic, after all. Now more, younger ambitious and competent people will see your successful alumni and want to follow a similar path. As this process continues, you have the added benefit of being as selective as you want, driving down your acceptance rate and therefore making yourself appear more prestigious.

This only works, though, if performance of the organization is somehow tied to outcomes. As soon as outcomes and performance become unhinged, you’ll see a breakdown in the system.

Fundamentally, I think this process applies to VC funds, too. Our job is to go find people who will likely be successful at what they’re working on (or for very early stage funds like my own, even on whatever it is they work on) and back them. There are some things we are good at -- just like universities are good at some things -- but most of the onus falls on our alumni.

The best VC funds know this. People want to get backed by top-tier funds because it’s a signal that they are likely going to succeed. Just like getting into an Ivy League school is a signal that you will succeed at other things in life, getting backed by Sequoia or a16z or Kleiner Perkins is a signal that you are more likely to succeed at building your startup.

Unlike universities, we actually pay a price if we are wrong. Unfortunately, an increasing number of universities either exist as hedge funds with real estate attached or as money laundering schemes with federal student loan money, or at the most anodyne, employment programs for an over-produced elite.

Power Laws & Returns

It’s not just enough to bet on somebody who would be successful at any old venture, though. If that were the case, VC funds would essentially be universities. No, the portfolio theory most VC funds operate by are fundamentally different.

You can imagine that a good university has a bell curve of alumni performance. Where the center of that curve falls on the general population is largely a function of the quality of the university’s signal. Stanford and Harvard will have a center that’s further to the right of the general population curve. A land grant state school that barely keeps itself afloat may be further to the left.

And that works well for most universities, so long as they continue to push to the right of the general population curve where their average falls.

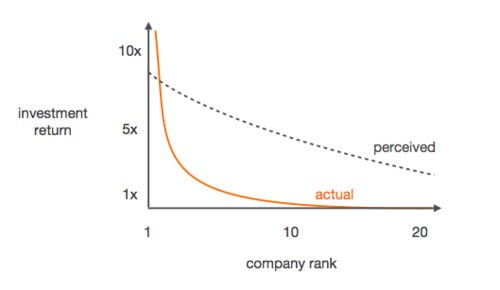

You might expect that that’s how a good investor works, too. You’ll get a few outlier, great returns, a few terrible returns, and everything else will do fine -- you just want the average to be a little above wherever the S&P 500 fell over the past couple of years.

That isn’t the case, though. Because your under-performing investments end up not merely getting you a little bit back but actually go to zero, and your investments that track the market are effectively zero, you need your outlier overperformers to really overperform.

This approach was well illustrated in Peter Thiel’s Zero to One, which pointed out that venture returns follow neither a normal distribution nor a Pareto distribution, but actually follow a power law distribution. Your winners don’t just need to outperform the market -- they have to outperform it several times over. That makes up for the losers and the average performers and gives you the profit you need to succeed.

For example, imagine you’re running a small, $10mm fund and you write 20 $250,000 first checks, for sake of simplicity of illustration. Estimating that 80% of your fund will get acquired for marginal profit for you, stay private as SMBs, or go to zero, that means $4mm of your fund is down the drain. Of your remaining 4 investments, 2 will double your money, taking you to $1mm, one will 5x your money, taking you to $2.25mm total. So you have $2.25mm returned from a $10mm fund. And remember, you want to 3x net your fund, so you really have $2.25mm returned from a $40mm target.

So how big does your home run have to be? It has to be such a home run that you turn $250,000 into at least $37.5mm. That’s a 150x ROI. That’s not just a homerun, that’s knocking a ball from Nationals park to San Francisco.

(This is assuming all but one company essentially goes to zero. In reality, you’ll probably need to turn $250,000 into $10mm and then a few other companies will make up for profits. Still, this isn’t easy (40x vs. 150x). Reality is a little messier — there’s follow-on funding and dilution, for example — but this is all just to illustrate power laws.)

So you have to back companies with big, insane narratives. The “we will change the world with this app” joke that you see trodded out to make fun of Silicon Valley really is what you have to look for.

The numbers in this illustration may seem pessimistic -- an 80% miss rate, really? -- but remember, startups are hard and you’re often investing when you have little more than a team and a relatively janky product to go on. And failure isn’t just going out of business -- it’s never going public or getting acquired, or being acquired for “undisclosed amounts.” Winning means a liquidity event like a big acquisition or an IPO.

So, yes, it’s hard. You have to look for monumental winners who will have an outsized impact on their industry and the world at large. It’s a far cry from the Index Fund approach of getting broad exposure to the entire market. And most people fail at it.

That all being said, venture is fundamentally a bet on the future. Do you believe that the future can and will be better -- or at least that people out there can work as lights that crowd out darkness? Good talent identification projects are fundamentally optimistic. We aren’t innovators ourselves, but we bet on innovators. If you didn’t believe those people were out there, you’d just go be a pencil mover at Big Faceless Bank, Inc., or hoard gold and bitcoin in your basement with your Ron Paul books.

I’m an optimist. And I hope you can be, too. I’d like to challenge you to search for the lights out there -- the people who will crowd out the darkness. Support them. Connect them. And if you’re able to, become them.